Property to crash in 2022?

HOUSE PRICES have hit dizzying highs despite the UK’s crumbling economy and many now expect a full-blown crash this year. Yet a house price crash may be averted for a surprising reason.

As the cost-of-living crisis intensifies the doom-mongers are shouting about the dangers of a property crash again. Yet there are good reasons why that may not happen despite today’s growing uncertainties.

There are good reasons to be worried about the property market right now.

The average homeowner with a £224,000 mortgage is paying £1,000 a year more interest a year as result of the BOE hiking rates from 0.1 percent in December to one percent today.

Base rates are set to climb higher and many homeowners will struggle as every other household cost soars at the same time.

Banks and building societies are already marking down properties during mortgage surveys, knocking £20,000 or £30,000 off the valuation to protect themselves.

That makes it harder for borrowers to raise the money they need, forcing some to pull out of their purchase. Property chains could collapse as a result.

It’s undoubtedly a dangerous time for the housing market.

This had led to growing caution among buyers, sellers and lenders, according to the Royal Institute of Chartered Surveyors.

Estate agents report having to do a lot more legwork for sales, as prospective buyers take their time, Hargreaves Lansdown’s senior personal finance analyst Sarah Coles said.

Sources report that buyers are finding it harder to get mortgages, as lenders tighten affordability criteria. “This is causing some chains to fall apart, as many banks don’t think properties are worth their asking price,”

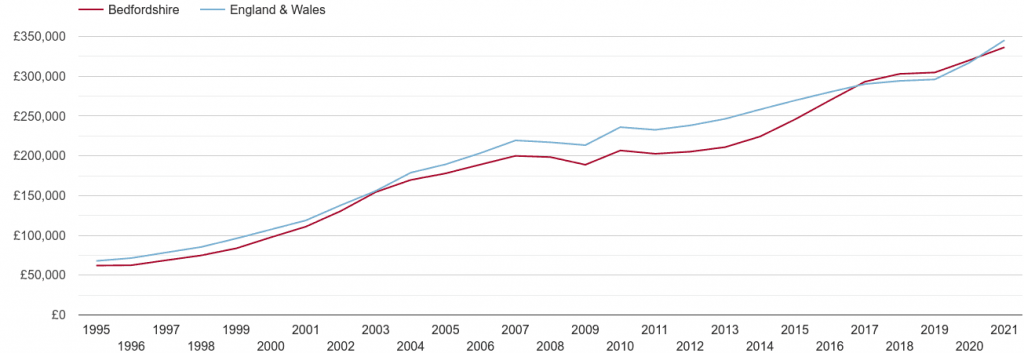

By every rational measure, today’s dizzying house prices should crash back to earth. The average property now costs an incredible 9.1 times the average salary in England, way above the long-term figure of four or five times.

First time buyers are struggling to build big enough deposits. Seven in 10 have now put their plans on hold for at least two years, Nationwide reports.

So why won’t prices crash?

One reason is that buyer demand is still strong, while the supply of property is weak.

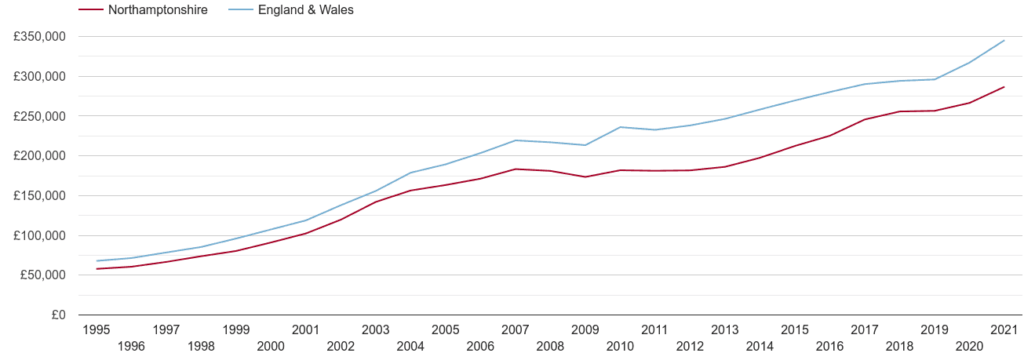

House prices jumped an incredible 10.8 percent in the last year, which includes a rise of 1.1 percent in April alone, adding £3,078 to the average home.

This has lifted the average property price to another new record high of £286,079, and Halifax managing director Russell Galley said activity shows “little sign of abating” amid strong buyer competition.

Demand continues to outpace supply due to the “insufficient number of new properties coming onto the market”.

Galley anticipates the rate of house price growth will slow, but only by the end of this year. He does not foresee a crash.

Another reason the market won’t crash is that owners are taking action to protect themselves from mortgage hikes, said Joshua Elash, director of property lender MT Finance. “They are increasingly locking into longer term fixed rates, in expectation of further rate rises.”

Also, mortgages remain dirt-cheap by historical standards. It is still possible to get a five-year fixed rate charging just 2.5 percent. When property prices crashed 20 percent between 1989 and 1993, mortgage rates hit a staggering 15 percent.

That would trigger the mother of all meltdowns today, but that isn’t going to happen.

Here’s the most unexpected reason why prices won’t crash.

If the UK is heading into recession, the Bank of England is likely to scale back its base rate hikes, said Rupert Thompson, investment strategist at Kingswood.

As a result, base rates may only climb to just 1.5 percent or two percent, still low by most standards.

This would keep mortgages affordable, and head off any crash. Incredibly, this means a recession could actually ride to the property market’s rescue. Few will have seen that coming.

There is also the fact that only around one third of properties in the UK are occupied by mortgage payers, the other third are owned outright with the remainder being rented. Of the third that pays a mortgage, many are on fixed term deals, with a few having fixed deals for five or ten years. The immediate effect will probably only be felt in the next year or two, until the rises in energy this year, which account for about 75% of the inflation figure, taper off.

There is a great possibility that interest rates will rise to as much as 2.5% by next year, though nothing is certain, then they will peak and gradually come down. The fact that there are some great long term fixed rates, indicates that those in the know, are confident that the rise in rates is only temporary, hence the reason they are offering to lock in good rates (for them) for a long time.

Another factor that differentiates the current climates from the pas, is the supply of money. Since the crash of 2008, banks have not only been super careful with lending, but the gap, between the base rate and the variable mortgage rate has been higher than ever.

Previously, the gap was around 1% at the most, but for much of the last 14 years, the base rate has been around 0.5% but the variable rate has been as much as 5%, which is a mark up of 1,000% and since the pandemic, when the base rate was lowered to 0.1%, some lenders were still charging a variable rate of 5%, that is a mark up of 5,000%! So as you may gather, the banks are awash with money and the availability of funding, will invariably keep the market safe.

It seems like the doom-mongers may have to wait a little longer for the big crash.